The browser you are using is not supported. Please consider using a modern browser.

Clear, centralized data analytics for banking.

See the whole picture and bring your data to life with the industry’s preferred banking analytics platform built for better banking.

Schedule a DemoJust a few of the banks bringing their data to life with KlariVis.

Built for Bankers, by Bankers.

As veteran bank executives, we’ve seen first hand how cumbersome it is to access critical data across disparate systems. KlariVis is changing how banks use data analytics by providing one source to ensure data integrity and empower you with reporting that's consistent, timely and accurate.

Statistics

- ALL Cores & Systems

- Unlimited Users Per Bank

- 650+ Pre-Built Dashboards & Reports

KlariVis Advantage

The future of banking analytics starts here.

We believe that data-driven decision making is the key to success in today’s rapidly changing financial landscape. We’re committed to providing banks with the tools and insights they need to thrive.

Explore the AdvantagesHow we help

Empower strategic decision-making across your entire bank.

- Create a single source of truth across your disparate systems.

- Get insights in minutes, not hours, for more informed and timely decisions.

- Self-service access gives your team the data they need, when they need it.

- Enable your entire team to respond quickly to changing market conditions or customer needs.

- Eliminate errors and inconsistencies to ensure decisions are based on accurate, reliable information.

- Better manage credit risk by identifying trends that indicate higher risk.

Tour the Features

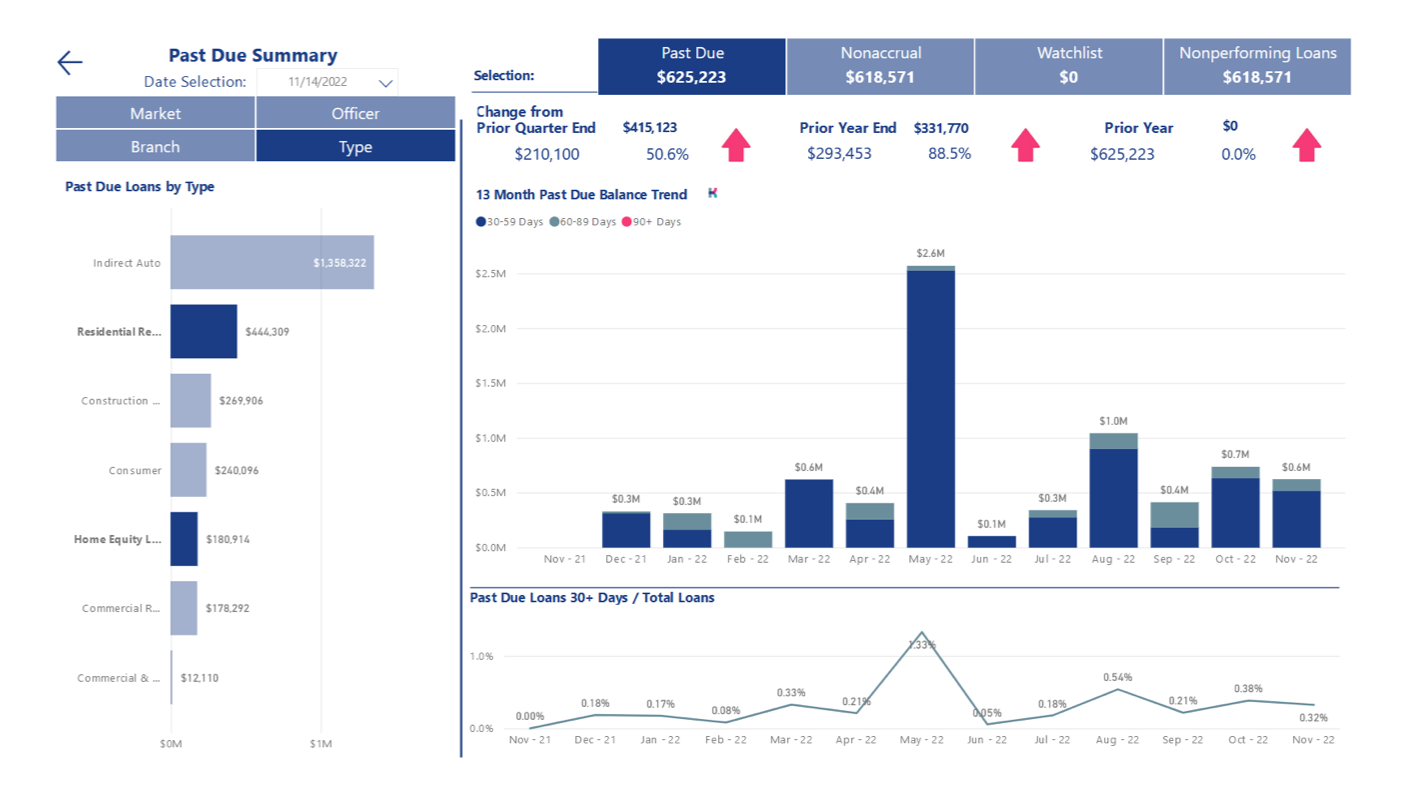

We deliver your data through interactive banking dashboards to give you immediate insight into key performance metrics that empower teams, drive profitability, and improve productivity at every level of the organization.

Interactive Dashboards

Empower your team to make informed decisions with self-service access to our 650+ interactive and static dashboards. Say goodbye to complicated reporting processes and hello to a more efficient and effective way of working.

Explore More Features

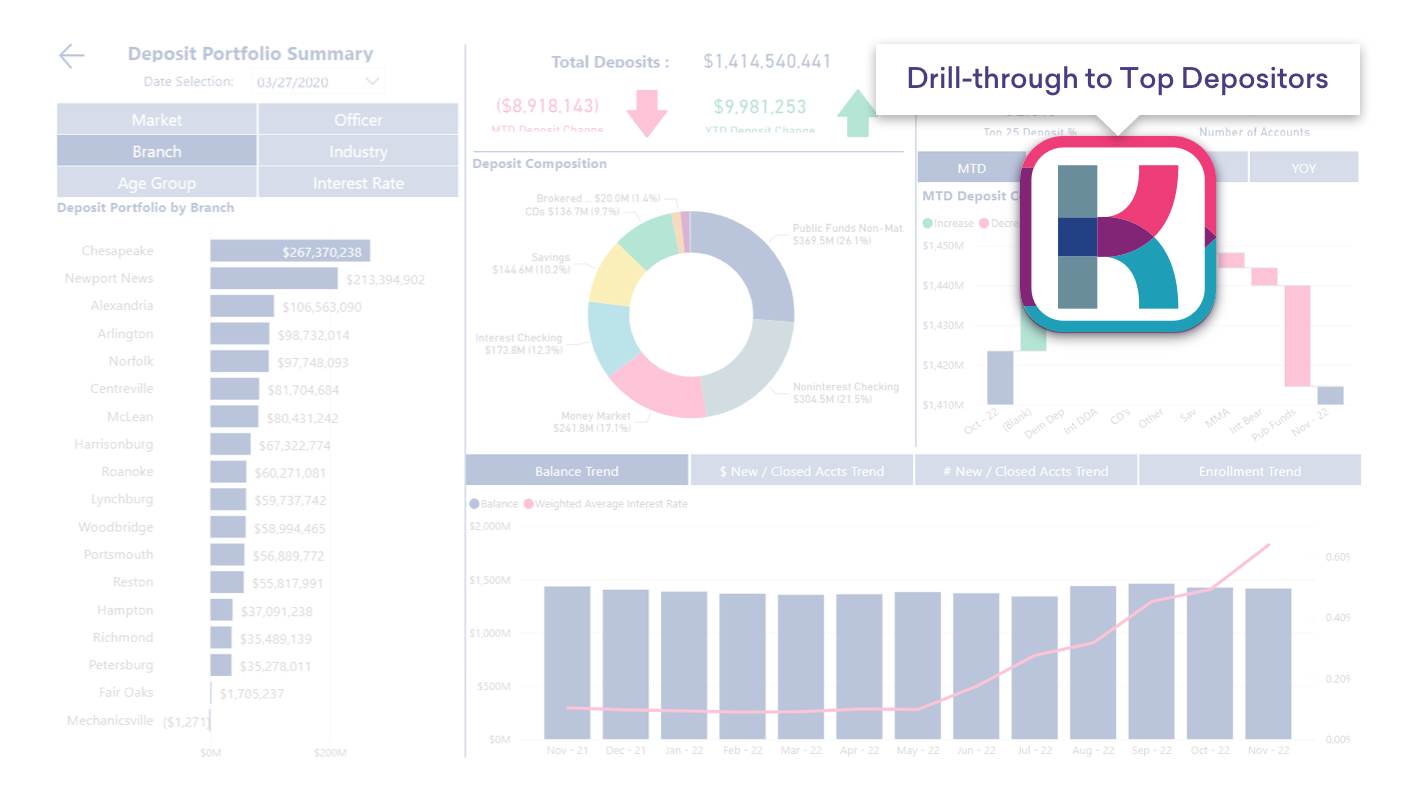

Customer-Level Drill Downs

Quickly drill down from a macro view all the way down to the customer level directly from your interactive dashboard. Instead of sifting through countless reports and making numerous phone calls, spend that valuable time taking action on the data rather than hunting for it.

Explore More Features

Enterprise Access

Gain insights into every aspect of your business, from lending and retail to finance and operations. With enterprise access, you can ensure that everyone in your organization has the data they need to make informed decisions and drive growth.

Explore More Features

Testimonials

Game Changing Efficiency

KlariVis has been instrumental in empowering

Merchants and Marine Bank to leverage data

effectively, make informed decisions, and

stay ahead in a competitive landscape.If you need a better handle on your data,

you NEED KlariVis.Casey Hill, Chief Financial Officer Big Bank Strength, Community Bank Heart

Discover how Citizens Bank of Edmond

leverages KlariVis to understand the

performance of their main bank and

ROGER, their digital bank for military

recruits, separately and together."Having KlariVis makes us feel like a big bank

even though we get to be small."Jill Castilla, President & CEO Data: A Guiding Light

Embark on KlariVis's journey to becoming an

ICBA Preferred service provider, showcasing

their data-centric, listener-first approach

tailored to meet banks' needs effectively.

KlariVis's emphasis on accurate data usage

is key, serving as a guiding light for banks

in their decision-making processes."The beauty about a company like KlariVis is

how efficiently and effectively they can get

their hands around the data and make it

actionable in a manner that meets the needs

of our community banks"Charles Potts, Chief Innovation Officer Level Playing Field

Since implementing KlariVis, the team at

Wayne Bank has spent far less time

searching for data and much more time

and energy serving their customers.KlariVis is going to take our small,

community bank and give us the

opportunity to be out in the field in

front of our customers more often.Jim Donnelly, President & CEO Transforming Data Management

By eliminating manual reporting and

providing universal data access,

KlariVis has empowered Village Bank

to enhance the client experience and

uncover new sales opportunities."It is very obvious that KlariVis is built

by bankers."Jay Hendricks, President & CEO Opportunities Identified

KlariVis has helped FNCB bank organize and

make sense of the mass amount of data that

they already had in their possession.KlariVis becomes invaluable.

Jerry Champi, President & CEO Staying Relevant

KlariVis has been a critical strategic

ingredient to Merchants' continued

pursuit of continued independence and

long-term relevance.KlariVis gives us so much hope.

Greg Evans, President & CEO Time Saving Clarity

FVCbank reduced past-due loans by 75% and

eliminated 60 hours per month in ad hoc

reporting.This is the first bank I have worked for in

30 years where I have data at my

fingertips when I want to see it, AND it’s

up to date!Bill Byers, Chief Lending Officer

KlariVis is the premier enterprise banking analytics platform for community banks nationwide.

Expert insights and informative events.

Become a Better Bank.

Stop guessing and start knowing by bringing your data to life.